I just tried your Overhead Allocation worksheet - Great Tool!

Bob Starinsky, IL

ACCOUNTING and FINANCE

What is Overhead Allocation?

Look at the typical Income Statement:

Overhead is comprised of the total of the items in the "Expenses" category that have not been allocated to a job on which the company is working.

Materials or subcontractor labor are easily assigned to a job. If they were delivered to the job or work was performed on a job...those expenses belong to that job.

But what about office rent or advertising or loan interest? Should those types of items be assigned to the individual jobs? If so, how should the allocation be calculated and applied? If not, how can you make sure that the Overhead Allocation Factor you am using in your estimates is neither too great (and you are losing work because your bids are too high) nor too small (and you are losing profit to cover overhead).

As a general rule, every expense that can be directly assigned to a job should be so assigned. This means that if you spent three hours today working on the Jones framing, along with the framing subs, you should bill that time directly to the Jones job, line item "framing labor costs". If your receptionist drove 80 miles round trip to pick up the interior doors for the Smith job, the time and the driving expense should be allocated to the Smith job.

OK, then.. the paper clip that is used to hold the contract pages together is charged to the client, the time spent in putting the contract in and addressing an envelope is charged to the client, the...wait a minute.

At some point, the benefit of knowing is outweighed by the cost of knowing. Once you have reached the point that the expenses involved in gathering information are greater than the value of that information,STOP.

The remainder of the expense information is then aggregated, and we have to find a way to deal with this remainder.

There is No Mandate to Allocate

I should point out that there is no business accounting mandate to do any kind of expense allocation at all. Generally Accepted Accounting Principles (GAAP) and Internal Revenue Service (IRS) generally require construction inventories to include a proportional share of indirect costs, but your accountant should be able to provide an adequate number for your needs. This is usually accomplished by dividing your indirect costs by the number of closed units and charging that amount to the closed unit. Not very useful from a management standpoint, but it meets the requirements.

So How Do We Make The Information Useful?

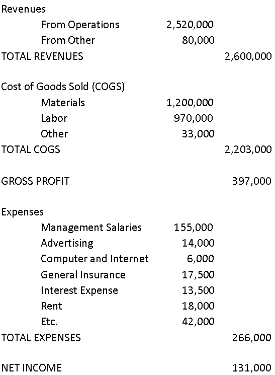

In absolute terms, the following Income Statements are equal in that they answer the questions the Income Statement is supposed to answer:

- 1) How much revenue did the business bring in?

- 2) How much money did the business spend to generate the revenue?

- 3) How much profit was left at the end of the period?

|

Income Statement Example 1  |

Income Statement Example 2  |

They may be equal, but they are not equally informative.

In the role of Financial Executive, the primary responsibility is to develop information which can be used to make and support financial decisions.

The Overhead Allocation process is within this primary responsibility of the Financial Executive. The more information we have about the impact of overhead expenses on company profitability, the better decisions we can make about estimating, purchasing, and hiring within the company.

Why Be Concerned About Overhead Allocation?

Estimating -While we are able to anticipate material costs to a high degree of accuracy, and labor costs to a manageable range, controlling indirect costs are more difficult. Items such as rents or, to a degree, utilities are knowable in advance, but there are always surprises such as increased insurance costs because of audits, unexpected equipment repairs, professional fees and so on that may show up. Paying attention to overhead costs and their relationships to other company benchmarks such as direct materials and/or labor costs, sales, or gross profits is imperative. Factoring those historical results into our estimates helps to ensure that the Overhead Factors we work with are as accurate as possible.

Purchasing -Understanding the impact of carrying costs (interest, opportunity costs, spoilage, waste, theft) on inventory can help determine whether or not we should take advantage of a sale to stock up on roofing or lumber. If you save 10% in lumber costs, but lose that same 10% plus 1% in inventory carrying costs, you are coming out behind.

Hiring -What is the effect on the overhead burden of bringing an employee on to replace a subcontractor? When you are comparing the compensation package for an employee (wages, benefits, slack time, increased payroll taxes), be sure to add in the cost of moving the labor cost from direct cost (subcontractor) to overhead (employee). The move from a variable cost to a fixed cost can have significant impact on your Overhead Allocation Factor, and may negatively affect your estimates.

More....

The next several pages address some other thoughts regarding overhead allocation.

First, a change to your Chart of Accounts is suggested to enhance management decision-making. |

Then we consider some alternative overhead allocation models, and discuss the pros and cons of each. |

Third, we look at a smoothing model based on Cost of Goods Sold for allocating indirect expenses that offers answers to some, if not all, of the overhead allocation issues raised by the other models. There is a free download available for this model. |

Finally, we review another model based on Dollars per Job Day which also offers an interactive template for you to download and try in your business. |

Be sure to take advantage of all of these resources. |

|

Return to ----> |

|

More about...

Related Topics

|

|

|

|

|

|

|

|

|

|

|

|

| Copyright © Builder-Resources. All rights reserved. Used by permission. |

Builder-Resources.com Builder-Academy.com Builder-BOS.com |

Design by: |